Consultancy Position: Data Architect

ZSL’s Sustainable Business and Finance programme is seeking a consultant to support the delivery of SPOTT’s launch of the 2022 timber & pulp SPOTT assessments, managing My SQL data exports, manipulation and imports using ProBench, MyPhpAdmin, and WordPress.

SPOTT Assessments

ZSL (Zoological Society of London) is an international conservation charity working to create a world where wildlife thrives. From investigating the health threats facing animals to helping people and wildlife live alongside each other, ZSL is committed to bringing wildlife back from the brink of extinction. Our work is realised through our ground-breaking science, our field conservation around the world and engaging millions of people through our two zoos, ZSL London Zoo and ZSL Whipsnade Zoo.

SPOTT is a free online platform supporting sustainable commodity production and trade. By tracking transparency, SPOTT incentivises the implementation of corporate best practice. SPOTT assesses commodity producers, processors and traders on their public disclosure regarding environmental, social and governance (ESG) issues. SPOTT scores tropical forestry, palm oil and natural rubber companies annually against over 100 sector-specific indicators to benchmark their progress over time. Investors, buyers and other key influencers can use SPOTT assessments to inform stakeholder engagement, manage ESG risk, and increase transparency across multiple industries.

Assessments are published three times a year, once per commodity, along the following timeline:

- Natural rubber: March

- Timber & pulp: July

- Palm oil: November

Tasks

The consultant will deliver the launch of the 2022 timber & pulp SPOTT assessments. The assessment launch tasks include:

- Create Probench “Export” Dataset based on the Survey Template

- Generate Probench “Export” dataset & download corresponding CSV file

- Generate 3 CSV files (using SPOTT admin page) from Probench CSV file and send to SPOTT team for editing

- Import of 3 CSV files in SPOTT database (using SPOTT admin page)

- Import of the Indicators, media and engaged companies CSV to the database via PhpMyAdmin

- Create the indicator categories for the commodity in the database

- Test templates to be updated on the SPOTT website to see the data

- Make sure data are visible on Test pages (and not on live pages) for SPOTT team to review

- Update the Assessment Summary Test template

- Update of the test templates with URLs and other texts changes

- Preparation for the release (updating production files without uploading)

- Release – Upload of all the production templates on the SFTP server

- Release – Database update (companies/assessments, publish = “Y”)

NB: The SPOTT website is a WordPress website running on PHP7.4, with a custom theme and a few custom plugins, HTML/CSS is used for the front end, with some JavaScript and AJAX interactions. The SPOTT website is linked to two different MySQL databases, one is supporting the WordPress website itself and the other is containing all the company/assessment related data displayed on the SPOTT website.

Required skills, experience and knowledge:

ZSL are inviting proposals from individuals or organizations with experience in the following:

- WordPress

- MySQL and PhpMyAdmin

Submission guidelines and requirements:

The candidates must submit the following:

- A short (<200 word) proposal, outlining their suitability for the contract, including relevant experience working with similar programmes.

- A cost proposal based on an hourly rate and an estimate of the number of hours required to complete the task

- CV

- Examples of previous relevant work

- Proposals must be received by 23rd May to be considered.

- Proposals should be submitted to David.Johnston@zsl.org for consideration.

- ZSL reserves the right to amend the scope of this RFP in order to get the most suitable consultant.

Contract Value

- Candidates should propose an hourly rate and provide an estimate of the number of hours required to complete the task

- NOTE: Consultants will be prioritised if providing better value for money i.e. by proposing a lower hourly rate

- NB If successful, the consultant may be considered for future assessment launches.

No expenses are foreseen. However, the consultant may present suggested expense required to deliver the contract for consideration by ZSL.

Contract Timelines

The timeline of the timber & pulp assessment launch is planned as follows (subject to change):

| Task |

Timeline |

| Consultant starts preparation of CSV export files from Probench |

Wed 1st June |

| Consultant to export CSV files from Probench and send to ZSL |

Mon 4th July |

| ZSL sends back files to consultant for upload to SPOTT |

Friday 8th July |

| Consultant publishes data on staging site for ZSL review |

Wed 13th June |

| ZSL reviews data and provides feedback to consultant on final updates |

Wed 13th – Fri 15th |

| Assessment launch to live site |

Mon 18 July |

The timeline for awarding the contract is as follows:

| Task |

Timeline |

| Proposal submission |

23rd May 2022 |

| Selection of consultant |

23rd-27th May 2022 |

| Contract awarded |

31st May 2022 |

| Work to commence |

1st June 2022 |

| Project completion |

20th July 2022 |

NOTE: Consultants are expected to pay all applicable local taxes. Where applicable, these should be included in the net cost provided to ZSL.

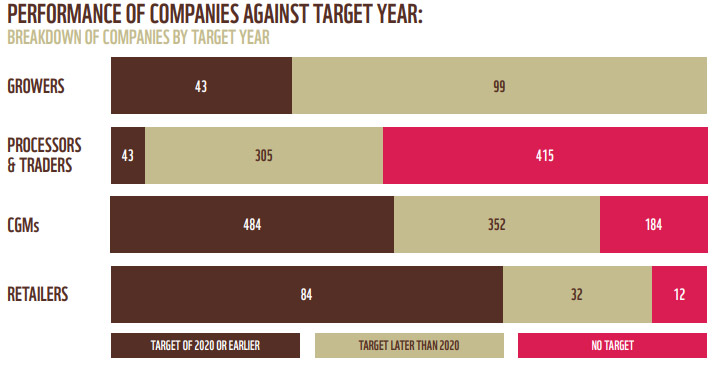

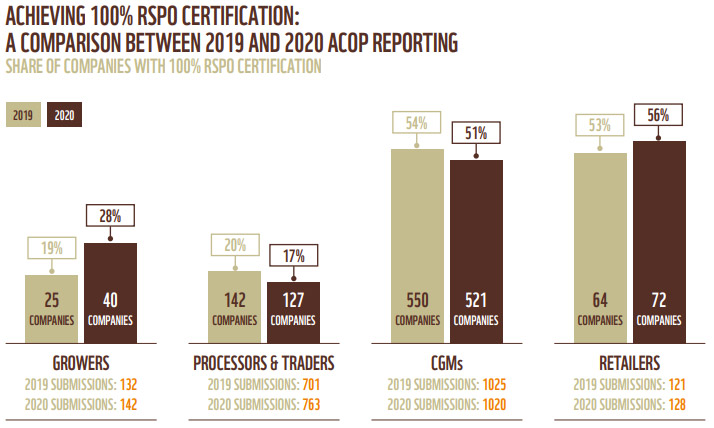

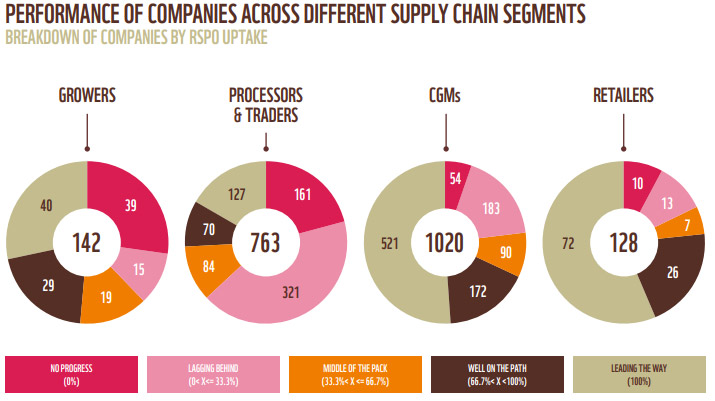

In this third edition of ‘Committed to Sustainable Palm Oil?’, ZSL and WWF analysed Annual Communication of Progress (ACOP) reports submitted by palm oil growers, processors and traders, consumer goods manufacturers (CGMs) and retailers for the year 2020. Some key findings of this year’s analysis were that:

- 2020 was supposed to be a crucial milestone for progress on sustainability and halting deforestation in the palm oil sector. However, while several companies have made progress in meeting their commitments to be 100% RSPO-certified by 2020, many RSPO members across the supply chain still have not even set targets.

- The share of companies with 100% RSPO certification has improved between 2019 and 2020, particularly across growers and retailers. However, progress remains very variable both within and between supply chain segments.

- Companies with the largest land area and volumes of palm oil handled are still falling short on certification. All companies need to take immediate and meaningful action to close the certification gap, with additional responsibility for bigger players to rapidly and significantly increase their uptake of sustainable palm oil.

With rates of tropical deforestation, biodiversity loss and green house gas emissions continuing to rise, RSPO member companies across the supply chain need to act fast to set, strengthen and deliver on their commitments towards a sustainable palm oil industry.

ZSL and WWF urgently call on all RSPO members to:

- Increase awareness: Understand and embrace the Shared Responsibility requirements, and improve awareness

of these among other members.

- Improve reporting: Ensure clear and precise reporting of data in annual ACOP submissions, to allow improved

analysis of ACOP reporting across and within sectors – in particular by vertically integrated companies. A clearer

picture of current efforts on Shared Responsibility is essential to accelerating progress.

- Act on certification: Implement the Shared Responsibility requirements and work towards increasing certified

production and meeting the latest uptake targets, as relevant to each supply chain segment, and continue to

strengthen these requirements over time.4

- Collaborate for progress: Work collectively, embracing the principle of Shared Responsibility, to drastically

improve efforts towards the production and sourcing of 100% RSPO-certified palm oil.

For more information, please contact:

Eleanor Spencer, ZSL-London, spott@zsl.org

Mai Lan Hoang, Engagement Manager, WWF-Singapore, mlhoang@wwf.sg

Key Findings at a glance:

As part of the PRI-coordinated engagement on Sustainable Palm Oil, more than 62 investment organisations with approximately US$8 trillion in assets under management endorsed a statement laying out their expectations of companies operating across the palm oil value chain and highlighting their continued support for a sustainable palm oil industry. https://www.unpri.org/download?ac=10612

During the collaborative engagement, the investors encouraged the companies they invest in to adopt responsible practices, including:

- To become members of the RSPO and apply the RSPO’s Principles and Criteria;

- To adopt and implement a publicly available No Deforestation, No Peat and No Exploitation (NDPE) policy, regardless of their certification status;

- To commit to full traceability of the palm oil they source and supply to the plantation level, and to participate in supply-chainwide transparency efforts by mapping and disclosing their palm oil concession areas;

- To set time-bound plans and regularly report on progress and practices;

Companies associated with unsustainable palm oil face a multitude of risks – operational, financial, regulatory and reputational – and these risks can cascade on to consumer goods companies and retailers further down the supply chain, as well as companies’ financiers.

Each year SPOTT publishes assessments of palm oil producers, processors and traders on their public disclosures on Environmental, Social and Governance issues. SPOTT palm oil assessments follow a comprehensive framework of over 180 best practice indicators spread across 10 categories.

The “PRI expectations score”, assessing companies against the PRI “Investor Expectations on Sustainable Palm Oil”, is generated by ZSL from a subset of SPOTT indicators. Investors can use this to assess companies against the expectations set out in the Investor Expectation Statement on Sustainable Palm Oil. A full score indicates that the company has key policies and commitments in place aligned with the expectations, but company policies and commitments may not translate into effective implementation on the ground and additional indicators should be used to appreciate a company’s approach in more depth.

For a more detailed and nuanced view of company disclosures, users are encouraged to review assessments in full on SPOTT.org and engage with companies and third parties directly. The SPOTT media monitor on each company page may provide some contextual information; however, independent due diligence activities should include measures to assess levels of implementation.

Company reports

Download all reports here, or select individual reports below:

The UK Environment Act 2021 sets out an important new suite of measures to tackle imported deforestation, by requiring companies to implement due diligence systems (DDS) for forest risk commodities in their supply chains. Whilst importing companies have been legally obliged to have DDS in place for timber and wood-based products since the introduction of the EU Timber Regulations (EUTR) in 2013 (now UKTR in the UK), new legislation means responsibilities will extend to companies buying other commodities associated with widespread deforestation.

Land-use change, including habitat loss and degradation is the leading driver of biodiversity loss globally (ZSL, 2020). Tropical deforestation is also the second largest anthropogenic source of CO2 and a significant proportion of these emissions are driven by international trade (Global Environmental Change, 2019). Seven key commodities are responsible for an estimated 65% of annual tropical deforestation risk within UK supply chains (JNCC, 2021). These are cattle (beef and leather), cocoa, coffee, maize, palm oil, rubber, and soy. As such the proposed due diligence regulation on forest risk commodities aims to reduce the UK’s imported deforestation footprint.

ZSL’s Sustainable Business and Finance team are committed to boosting corporate best practice and welcome the new legislation, however the government must work to ensure secondary legislation is both robust and ambitious. Deforestation risk is complex and dynamic, and legislation must be flexible enough to adapt to new challenges or new deforestation drivers as they emerge.

We have recently responded to Defra’s open consultation on ‘Implementing due diligence on forest risk commodities’, which sought input from stakeholders on how the new requirements should be rolled out. Many important elements of the scope of requirements are currently undecided, in particular the commodities being legislated for and the criteria for which companies are or are not included.

We call on the UK government to:

- Include a broad scope of commodities from the start, at a minimum covering the proposed seven; cattle (beef and leather), cocoa, coffee, maize, palm oil, rubber, and soy

- In addition to these, aquaculture and other sectors that drive deforestation of vital mangrove habitats should also be considered.

- Utilise current understanding of trends and projections, to ensure inclusion of commodities which may have small but expanding footprints.

- Regulate all companies in forest-risk commodity supply chains, irrespective of turnover, whilst expecting large companies to do more, in line with their sourcing volumes and capacity to leverage change.

- Set ambitions for the regulation to extend beyond legality by integrating other sustainability indicators. A narrow focus on legality not only misses the well-known issue of ‘legal deforestation’, but may even disincentivise producer countries from improving governance structures that would raise the standard of ‘legal deforestation’

We recommend companies start preparing for the new requirements now, by introducing sustainable sourcing policies and mapping their supply chains. As the focus of due diligence is risk mitigation and risk avoidance, companies should engage suppliers and invest in their supply chains to drive meaningful change at producer level to tackle risk ahead of legislation entering into force.

ZSL will be following the outcome of the consultation closely and encourage others to do the same. We believe this legislation is a vital piece of the puzzle to reduce commodity-driven deforestation and ensure a world where wildlife thrives.

For more information, see https://consult.defra.gov.uk/international-biodiversity-and-climate/implementing-due-diligence-forest-risk-commodities/

A guide to setting robust policy commitments and reporting on practice in soft commodity supply chains.

This guide is designed to help companies set and report on robust gender equality commitments across all operations, including in relation to management, employment and interactions with communities. It is relevant whether you are a producer, processor, trader or buyer of products in soft commodity sectors.

Gender equality refers to the “equal enjoyment by women and men of rights, opportunities, resources and rewards. A critical aspect of promoting gender equality is the empowerment of women, with a focus on identifying and redressing power imbalances.”

SPOTT assesses soft commodity companies on their public disclosure of gender policies.

This Thematic Guide from ZSL provides an overview of the importance of taking gender into consideration during policy-making. Other Thematic guides in the series include:

Thematic Guide No. 1 to Zero Deforestation

Thematic Guide No. 2 to Traceability

Thematic Guide No. 3 to Supplier Engagement

Thematic Guide No. 4 to Free, Prior & Informed Consent (FPIC)

Thematic Guide No. 6 to The Living Wage

Thirteen leading rubber manufacturers including Michelin, Pirelli and Top Glove, are ranked in a new assessment led by ZSL SPOTT. This analysis covers the companies’ public policies and commitments relating to environmental, social and governance (ESG) issues – a world-first for the rubber manufacturing industry.

The manufacturers were among 30 natural rubber companies, including producers and processors assessed by SPOTT’s team in research published today (2 March 2022) as part of ongoing efforts to encourage transparent supply chains and a greener and fairer future for rubber.

70% of the world’s natural rubber is bought and utilised for tyre production. The global demand for rubber, harvested from plantations of the rubber tree (Hevea brasiliensis), has led to more than five million hectares of deforestation in recent years.

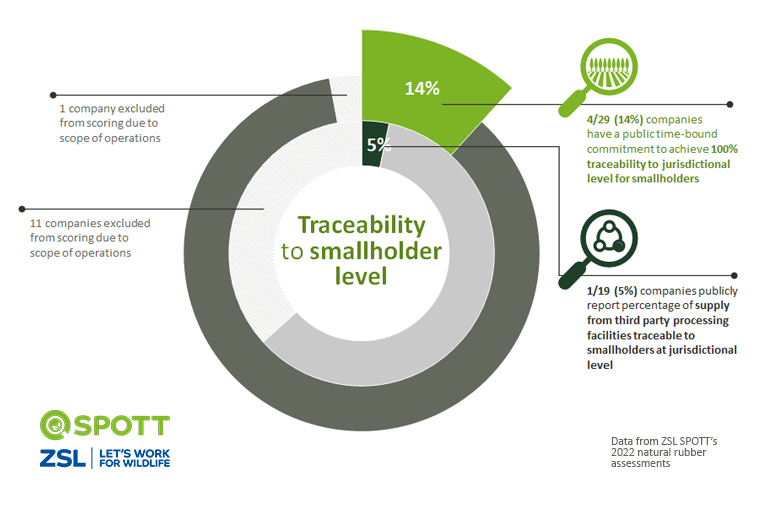

ZSL’s research showed only 14% (4/29) of companies commit to trace all rubber sourced from smallholders (small scale farmers) back to its place of origin by a target year. Meanwhile, 5% (1/19) of manufacturers and traders publicly reported the percentage of their supply from third party processing facilities traceable to smallholders at the jurisdictional level.

This freely available data highlights a significant challenge for the sector – a lack of traceability of natural rubber from smallholders who produce around 85% of the world’s natural rubber. Smallholders can face exploitation and human rights violations in long, complex supply chains that are often hard to trace. This lack of visibility at the commodity’s source makes it nearly impossible for companies downstream to claim rubber is cultivated in a sustainable way.

Sam Ginger, ZSL’s lead analyst on the study, said: “Companies should move quickly to scale up efforts to map entire supply chains so sustainability commitments can be implemented from farm to factory.

“Rubber companies have a responsibility to ensure farmers who are vulnerable to fluctuating demands and market conditions are not exploited, and to protect the biodiverse ecosystems where they operate and source their rubber.”

Most rubber is harvested in southeast Asia, such as Thailand and Indonesia, with the Asian continent accounting for 85% of global production. Tropical regions, where natural rubber trees are grown, are home to a high diversity and abundance of animal and tree life, vital resources for local and indigenous communities. They also help maintain global climate stability.

The team’s research showed that 62% (18/29) of companies that source from smallholders had a clear public commitment to zero-deforestation applicable to all their suppliers, but just 10% (3/29) publicly reported some evidence of monitoring deforestation and/or ecosystem conversion in supplier operations. The study revealed that rubber manufacturers scored higher than producers and processors, with an average of 42% compared to 37%. Michelin, assessed as a producer, processor and manufacturer of natural rubber, scored highest of all with nearly 82%.

Amy Smith, sustainable natural rubber program director for forests at World Wildlife Fund (WWF) in the US, said: “The SPOTT data shows the rubber industry’s wide gap between policy and action. The company that produced your vehicle’s tires is likely unaware of the natural rubber’s origin or the impact of its production.

“New and upcoming legislation in the EU and US will require companies to know. They must understand where their natural rubber comes from and demonstrate it did not result in deforestation or human rights violations. WWF urges investors to take note and reward companies that are going the extra mile by tracing rubber from farm to factory and ensuring that production meets rigorous ESG criteria.”

Sam continued: “We recognise that companies are at different stages of their sustainability journey but hope that the participation of such high-profile brands will set a precedent for others working in the supply chain. We also strongly urge manufacturers to help their suppliers improve on their ESG transparency.”

Natural rubber plantation – Indonesia (Photo: David J Johnston, ZSL)

Companies who were members of the Global Platform for Sustainable Natural Rubber (GPSNR), a multi-stakeholder platform for natural rubber sustainability with over 150 members, scored higher in their transparency and public commitments than those that weren’t, with an average of just over 52%, compared to 25% for non-members.

Stefano Savi, director at GPSNR, said: “I am glad to see GPSNR members performing well, I think there is room for improvement, and it is good that GPSNR will have reporting requirements for members from this year, which will position GPSNR members well to achieve an even better score in next year’s report.”

Assessed companies are encouraged to work together with SPOTT analysts during the consultation period when they have an opportunity to improve their scores before ZSL publishes its results on the platform. This year, every company that engaged with ZSL improved its score by disclosing more information on its website during the assessment process.

Sam concluded “we would like to see more suppliers engaging with ZSL SPOTT and GPSNR to ensure public commitments are being made, implemented, and reported on across the whole supply chain. Working together would go some way towards a scenario where sustainable and equitable production of natural rubber can continue whilst enabling the recovery of wildlife within the landscapes it occupies.”

ZSL urges governments to ensure nature is part of wider policy decision-making. ZSL and partners are supporting improved due diligence processes for forest risk commodities in the UK Environment Act, and ZSL is calling for natural rubber to be included in EU legislation. Governments should prioritise biodiversity loss and recognise its interconnections with other environmental issues such as climate change. You can support ZSL global science and conservation work by donating at www.zsl.org

Rainforests in Southeast Asia (Photo: David J Johnston)

SPOTT assesses the most impactful producers, processors and traders in the timber and pulp sector on their public disclosure regarding the organisation, policies and practices related to environmental, social and governance (ESG) issues.

Assessed companies are reviewed on an annual basis to ensure that their inclusion continues to align with this aim and with the needs of our users. The review process includes desktop research as well as consultation with our Technical Advisory Groups. Our selection process takes into account a variety of factors, including the location and extent of the producing and/or processing operations, nominations by interested stakeholders, companies that have volunteered for assessment, evidence of unsustainable practices identified through media reports, and donor expectations.

Two companies removed from SPOTT in 2022

- CENIBRA (assessed since 2018) – will now be assessed under its new parent company Oji Holdings Corp

- Sodinaf (assessed since 2019) – management of its concessions has been taken over by other companies in the region.

All previous assessments of these companies will remain accessible through the SPOTT website.

Two new companies selected

The removal of CENIBRA and Sodinaf allows for the inclusion of two new companies. In line with our company selection process, we have identified two key companies to include for the 2022 assessment, based on their significant land holdings in priority countries and nominations by interested stakeholders.

- Société de Transformation du Bois de la Kadey (STBK) – manages a significant landbank in Cameroon

- Bornion Timber Sdn Bhd (BTSB) – manages a significant landbank in Malaysia

Other changes to SPOTT-assessed companies

- SEEF (assessed since 2019) – will now be assessed under its parent company F Jammes SAS

- Sodefor (assessed since 2017) – will now be assessed under its parent company NorSud Timber

All previous assessments of these companies will remain accessible through the SPOTT website.

ZSL has notified the selected companies regarding their forthcoming assessment on SPOTT. SPOTT assessments of timber and pulp companies began in April and companies were contacted with their draft assessments in May/June, providing them with the opportunity to make further disclosures ahead of the final review and publication of assessments. Final assessments will be published on SPOTT in July 2022.

At least a quarter of the world’s land area is owned, managed, used, or occupied by indigenous peoples, encompassing up to 80% of the planet’s biodiversity. Indigenous and local communities can and should be essential partners in the conservation of forest ecosystems and their inherent biodiversity. More than 90% of Indigenous Peoples’ and Local Communities’ (IPLC) lands are in good or moderate ecological condition.

From an estimated global rural population of 3-4 billion, about 1.3 billion forest-dependent people live in forest landscapes as Indigenous Peoples or Local Communities (IPLC), and several studies suggest that cooperation with IPLC for conservation purposes has positive impacts on the ecological condition of forest ecosystems and their inherent biodiversity values.

Positive outcomes for both community livelihoods and conservation come from cases where Indigenous peoples and local communities play a central role, such as when they have substantial influence over decision making or when local institutions regulating tenure form a recognized part of governance. “In contrast, when interventions are controlled by external organizations and involve strategies to change local practices and supersede customary institutions, they tend to result in relatively in-effective conservation at the same time as producing negative social outcomes.”

Despite their role as the main stewards of the world’s forests and biodiversity, IPLC lands are under increasing pressures due to commodity-driven industries such as timber and pulp or industrial agriculture, with potential negative impacts. In this regard, ZSL believes that sustainable forest management requires a meaningful commitment to securing IPLC rights and land tenure and guaranteeing Free, Prior, and Informed Consent (FPIC). Hence, the logging industry has a fundamental responsibility to engage indigenous and local communities in timber and pulp value chains, while facilitating sustainable development and biodiversity conservation in forest production landscapes.

This report looks at the potential for the timber and pulp sector to contribute to securing IPLC rights in forest production landscapes, drawing on key findings of the analysis of data from ZSL SPOTT’s 2021 assessments of 100 timber and paper producers, processors and traders, looking at key environmental, social and governance (ESG) issues.

ZSL is strongly urging timber and pulp supply chain actors to publicly disclose all of their sustainability policies so buyers, financial institutions and other stakeholders can assess the quality of corporate commitments.

Downstream companies and financial institutions hold the key to driving significant environmental and social changes in the natural rubber industry by committing to and applying sustainable practices and improving sourcing procedures.

Natural rubber is extensively used worldwide for everyday products such as tyres, shoes, footballs, condoms, gloves, sponges, roads, and balloons. On average, the annual consumption of rubber per person is estimated at 3.5 kg.

While natural rubber production can have significant environmental and social impacts, it can be grown sustainably, providing a livelihood for millions of people. Natural rubber production has been under the radar for many years in terms of its impacts, with other commodities such as palm oil and soy historically under more pressure to improve practices. But this is starting to change with the formation of the Global Platform for Sustainable Natural Rubber (GPSNR) and an increasing number of companies committing to producing and sourcing sustainable natural rubber.

This report contributes to this sustainability movement in the natural rubber supply chain by providing key findings of the analysis on data from the 2021 SPOTT assessments of 15 natural rubber producers and processors, looking at key environmental and social issues.

ZSL urges increased company disclosure of sustainability information on operations, policies, and practices. This includes companies adopting sound and robust Environment Management Systems, best practices of human rights and labour rights, good agricultural practices, NDPE policies, improving transparency and traceability in their supply chain, disclosing, and regularly reporting progress on implementation of their sustainability policies. Using the list of key SPOTT indicators (see section 6 in the report) can be an effective starting point.

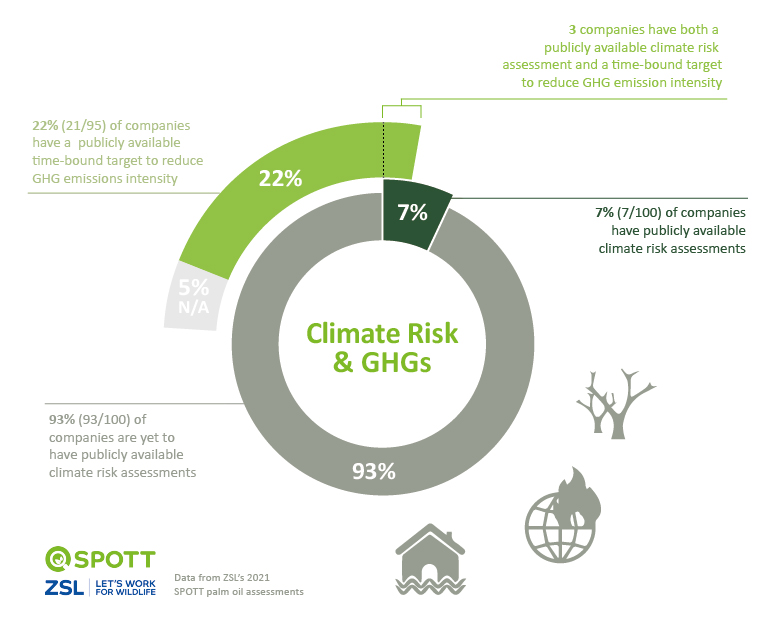

ZSL is urging the palm oil industry to take climate change seriously and play its part in tackling the world’s climate and biodiversity crises, as it publishes its annual assessment of 100 of the world’s most significant palm oil companies.

ASSESSMENT SUMMARY

The analysis of 100 producers, processors and traders of palm oil found that only seven companies have conducted and published an assessment of the risks posed to their business by climate change. Compiled by ZSL’s SPOTT team – an initiative developed by ZSL to incentivise transparency of reporting and the implementation of best practice – the results show just how slow the palm oil sector has been to act. This comes despite the industry being described as ‘highly exposed to global and local climate transitions’ in a recent report by Orbitas, due to the industry’s high export volume, reliance on land and use of emissions-intensive fertilisers and diesel fuels.

Modelling done by Orbitas, using the scenario of global average temperature rising 1.5°C above pre-industrial levels, projects that demand will outpace supply due to population growth and increasing demand for bioenergy. This will push palm oil prices and land value up, increasing pressure on producers to intensify production and putting the environment at even greater risk – unless producers move swiftly towards sustainable low carbon techniques.

Eleanor Spencer, ZSL’s Sustainable Business Specialist for Asia says: “As demand for palm oil increases, so will the pressure on land managers to improve production at all costs. These production increases are likely to come from the spiralling use of emissions-intensive fertiliser, which can have negative effects on water quality and catastrophic consequences for local communities and wildlife.

“Increased demand and higher prices for palm oil also bring with them a higher risk of corruption and forced labour. It is therefore crucial that palm oil companies put in place climate-risk strategies now so that future demand can be met in the most sustainable way possible.”

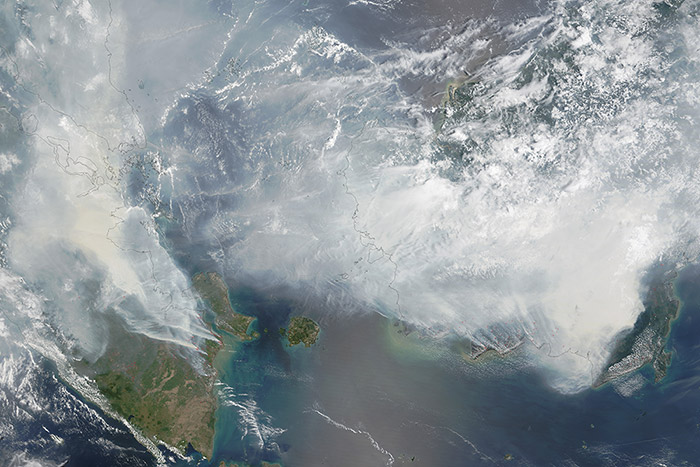

Unsustainable palm oil production is one of the biggest contributors to habitat loss in the tropics as it involves clearing and burning forests and peatland to make way for palm oil plantations. The process of deforestation also contributes to the acceleration of climate change, as does the draining of carbon-rich peat swamps which, once drained, release the stored carbon into the atmosphere. A study published in Nature in 2020 found that the conversion of peat swamp into palm oil plantations in Southeast Asia alone contributed up to 0.8% of total global GHG emissions – the equivalent of almost half of the aviation industry.

Fires and smoke across Indonesian Islands of Sumatra and Borneo as rainforests are cleared for palm oil. [NASA image by Adam Voiland (NASA Earth Observatory) and Jeff Schmaltz (LANCE MODIS Rapid Response). 2015]

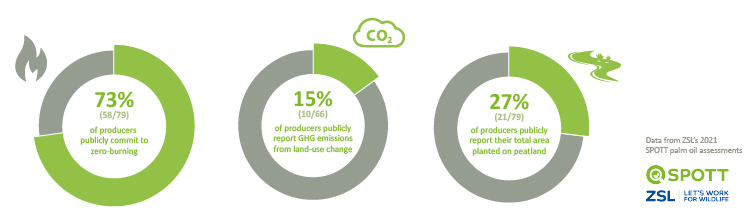

The industry has made progress in this regard – of the palm oil producers assessed by ZSL’s SPOTT team, 70% have committed to zero deforestation, 68% have committed to no planting on peatland and pledges have also been made by 59% to set aside areas for conservation.

Spencer said “Palm oil producers are significant contributors to global greenhouse gas (GHG) emissions themselves, and they risk shooting themselves in the foot – as well as accelerating biodiversity loss and contributing to climate-related issues faced by consumers across the world – if they don’t start taking climate change seriously.”

Sadly, while the appetite for ending unsustainable practices appears to be improving, the majority of companies (78%) have still failed to make a time-bound target to reduce GHG emission intensity. Transparency also remains an issue, with just 16% able to report on how they are monitoring and enforcing their zero-deforestation commitments with their suppliers, only 27% of producers reporting their total area planted on peatland and only 15% reporting GHG emissions from land-use change.

Hanah Chang, Engager, EOS at Federated Hermes (member of the SPOTT Supporter Network) says: “We engage with companies around the world, urging them to put in place strategies and targets aligned with a 1.5°C pathway and to play a role in reversing biodiversity loss. Commodity-driven deforestation is a major contributor to the climate and biodiversity crises so the palm oil value chain is an important area for engagement. Deforestation also often gives rise to concerns about human and labour rights, so we continue to ask companies to align to the UN Guiding Principles on Business and Human Rights and commit to the principle of Free Prior and Informed Consent (FPIC).”

Spencer concludes: “The urgency of the climate crisis has never been clearer or more widely acknowledged, and it is unacceptable that the palm oil industry – a significant contributor to that crisis – and those financing it still have such little access to quality disclosures to help quantify and address climate risks in this sector. Upstream palm oil companies that continue not to disclose this important information, or engage with NGOs and other stakeholders to improve, are putting at risk not only the many species, people and ecosystems threatened by the climate crisis, but even their own business, and those of their buyers and financiers.”

Found in many foods and household products, as well as being used increasingly in biofuels, palm oil has become a polarising topic because of its association with deforestation and habitat loss. However, palm oil can be produced sustainably and remains the most efficient major vegetable oil crop in terms of yield per hectare. Complete rejection of the product would likely create demand for a less efficient alternative and lead to further deforestation and habitat loss, which is why ZSL is working with partners and the industry to improve the sustainability of palm oil, including with the RSPO (Roundtable on Sustainable Palm Oil), the world’s largest palm oil sustainability certification scheme.

ZSL is calling on the palm oil sector, buyers and financiers to put in place effective strategies for dealing with climate change that will benefit business, the public and the environment.

ZSL is also urging world governments and policy makers to put nature at the heart of all decision making to effectively tackle the intertwined threats of climate change and biodiversity loss. ZSL’s scientists and conservationists called on world leaders to make this commitment at COP26. Find out more, and support this work by visiting zsl.org/natureatheart

Sumatran rainforest [photo by David J Johnston]