The Zoological Society of London’s (ZSL) SPOTT initiative is expanding to assess the transparency of major forest product producers operating in priority tropical areas, scoring companies on their commitments to environmental, social and governance (ESG) best practice. We have selected 24 companies for publication by November 2017.

Timber and pulp production – a growing problem

International trade in wood products represents a market worth billions of dollars per year. This market requires a huge input of raw materials from the world’s forests, with global demand for industrial roundwood estimated to reach two billion cubic metres per annum by 2030 – an increase of 25% in twenty years.

Growth in production will be underpinned by increased demand for wood products: with consumption of pulp and paper products set to more than double by 2060; and the market for solid wood products anticipated to increase by at least a quarter over the same period. As the supply of wood from developed countries is set to carry on falling as demand grows globally, forest nations in the tropical zone will likely play an ever more important role in production.

If managed appropriately, the world’s forests have the potential to provide these renewable commodities in perpetuity. However, growing global demand is pushing tropical countries to produce cheap timber and pulp through the unsustainable exploitation of primary forests and the development of fast-growing plantations in place of these natural forests. Such activities may jeopardise both the long term economic development of producer nations and the globally important environmental services provided by natural forest ecosystems – including carbon storage, watershed regulation, and biodiversity conservation.

Tools for responsible investment

In the past ten years, the shift towards more sustainable and responsible patterns of investment has been pronounced, with an increasing number of investment professionals making commitments to sustainable finance initiatives such as the UN Principles for Responsible Investment. The delivery of these commitments can be made more difficult by the operational and reputational risks faced by tropical zone forest product producers, particularly as the finance sector increases its exposure in these emerging markets. To mitigate these risks, investors can use the information provided by SPOTT to improve their engagement processes and inform the research which guides their investment decisions.

New ESG indicators and assessments

SPOTT currently assesses the public disclosures and commitments of palm oil producers to provide Environmental, Social and Governance (ESG) relevant information to investors, buyers and other stakeholders looking to fulfil their own commitments. SPOTT assessments for timber and pulp companies will provide users with a tried and tested toolkit for monitoring the transparency of key forest product companies operating in the tropics.

Corporate transparency will be assessed through an indicator framework that draws on established sustainable forest management best practice principles – for example, the identification and appropriate management of High Conservation Value (HCV) areas. By assessing publicly available information against these indicators, the new assessments will help stakeholders to monitor progress, support uptake of best practice and foster better on-the-ground outcomes.

SPOTT will focus on tropical forests given their extremely high species diversity, vital role in livelihoods, and importance as carbon sinks and stores. Forest loss due to fire and forestry is also greatest in the tropics. According to Supply Change, an estimated 53% of timber and 37-60% of pulp exports from tropical countries have displaced forests.

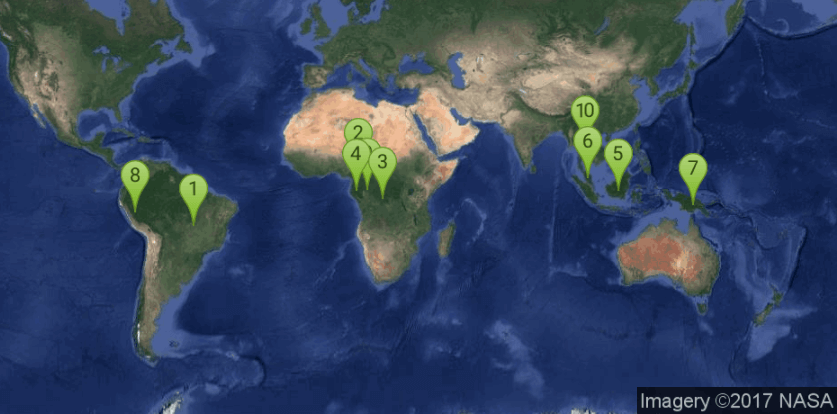

Country selection

To identify priority countries we applied a range of criteria to countries in the tropics such as amount of primary forest cover (FAO 2015), tree cover loss (GFW 2014 and FAO 2015), Industrial Roundwood production (ITTO 2014) and Intact Forest Landscape area (GFW 2014). We also considered the size of timber, pulp and paper industries within each country, and the extent to which they are driving deforestation. Our appraisal of deforestation risk made use of WWF’s Deforestation Fronts driver and threat assessments among other sources.

We identified 10 countries with large areas of high quality forest cover under threat from unsustainable timber and pulp production:

- Brazil

- Cameroon

- Democratic Republic of the Congo

- Gabon

- Indonesia

- Malaysia

- Papua New Guinea

- Peru

- Republic of the Congo

- Thailand

Company selection

With the list of priority countries selected, we identified key timber and pulp producers operating in these areas. We acquired an initial list of 383 companies provided by Bloomberg, refining the selection further by looking at those that specifically filed revenue from ‘forestry and logging’, ‘logging’ and ‘timber resources’. Other selection factors included location of operations, size of landbank and market capitalization.

SPOTT will initially score 24 timber and pulp companies, with a view to expanding this to 50 companies in future.

1. APRIL / RGE

2. Asia Pulp and Paper

3. Cikel Group</p

4. Interholco AG

5. Duratex S.A.

6. Groupe Blattner Elwyn

7. Groupe SEFAC

8. Groupo Jari

9. Klabin S/A

10. Oji Holdings

11. Olam International

12. Pallisco

13. Precious Woods

14. Rimbunan Hijau (RH Group)

15. Rougier SA

16. Samling Group

17. SLJ Global Tbk

18. Sodefor S.P.R.L.

19. Sumitomo Forestry

20. Suzano Papel e Celulose S.A

21. TA ANN Holdings Bhd

22. Toba Pulp Lestari

23. Vicwood Group

24. WTK Holdings Bhd

The first set of assessments for timber and pulp companies will be published in November 2017.

For more information and a full list of indicators and company details, please visit the assessment page for timber and pulp companies.