Find information about SPOTT’s methodologies below:

Company Selection Methodology

SPOTT assesses commodity producers, processors and traders on their public disclosure regarding their organisation, policies and practices related to environmental, social and governance (ESG) issues. SPOTT scores tropical forestry, palm oil and natural rubber companies annually against over 100 sector-specific indicators to benchmark their progress over time.

Click below to see the scoring criteria for each commodity:

| Palm Oil | Timber and Pulp | Natural Rubber |

SPOTT assesses companies operating in, and sourcing from, tropical forest landscapes due to their extremely high species diversity, their vital role in livelihoods, and their importance as carbon sinks and stores. We select companies of the greatest interest and impact in these landscapes given their operations and supply chain positions, as well as considering the needs of SPOTT users and if companies operate within priority geographies. (Priority geographies vary for each commodity, and depend on a number of factors, for example key commodity production areas, areas with high levels of biodiversity under threat, and areas that align with ZSL objectives and scope of funding). SPOTT aims to assess companies at the parent company level where relevant, as we expect these companies to have policies in place which apply to all of their subsidiaries.

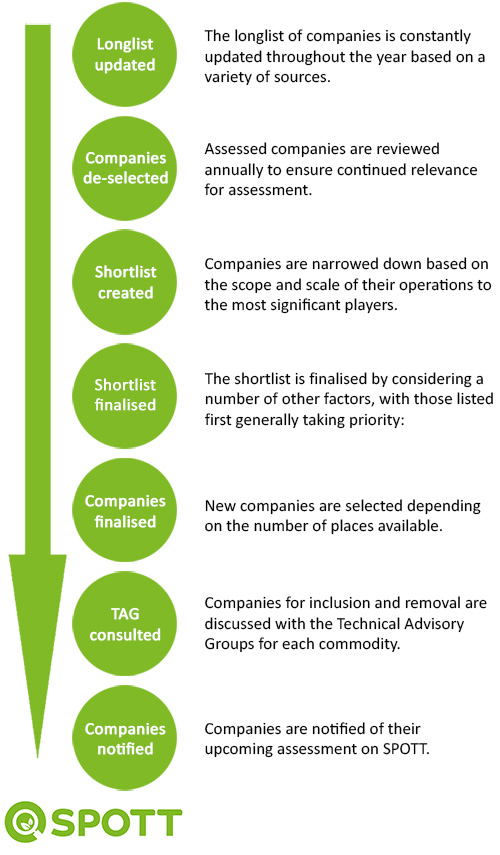

Assessed companies are reviewed on an annual basis to ensure that their inclusion continues to align with these aims and with the needs of our users. They are also reviewed to ensure they remain active in the assessed-commodity sector and that there have been no major changes to the scope and scale of their operations (i.e. significant reduction in landbank for production or volumes processed, or operations in certain countries sold). Changes are kept to a minimum and are made only when deemed necessary.

Our selection process considers a variety of factors, however, as SPOTT has evolved over time, and the demands of our users change, the company selection process has also adapted to align with this. In general, the scope and scale of a company’s operations are used to narrow down the shortlist of companies. Once the more significant operators have been identified, the following factors are considered, listed in order of importance:

1. Scope and scale of operations (e.g. areas of land owned or leased, volumes processed, market capitalisation)

2. Operations in priority landscapes

3. Allegations of unsustainable practices identified through media reports

4. Nominations by interested stakeholders, or companies volunteering themselves for assessment

5. Presence of a company website

6. Company already assessed on SPOTT under another commodity

As SPOTT is a transparency initiative with sustainability and conservation objectives, selection criteria must be balanced with impact opportunities, as well as the needs of its users and the scope of its funding. Therefore, selection priorities may change over time, and may require a certain qualitative element of review as well. More detail on these yearly changes can be found in the FAQs.

Companies to be included or removed are discussed with the Technical Advisory Groups before finalising and are then notified of their upcoming inclusion or removal.

External Verification

In 2019 SPOTT revised its indicator frameworks to place more emphasis on assessing progress reported by companies in implementing their commitments. The level of reporting on the implementation of these commitments is classified as follows:

- Self-reported

- Externally verified

- Verified through certification

ZSL places greater weight on second- and third-party verified information within these practice indicators while still rewarding companies for self-reported progress. This change in methodology was prompted by demand from stakeholders to increase SPOTT’s focus on implementation. SPOTT does not conduct on-the-ground verification but aims to capture where verification has already been conducted, including through relevant certification schemes.

SPOTT aligns with the Accountability Framework Initiative (Afi) on its definition of externally-verified information:

Self-reported: Reporting of compliance, performance, and/or actions taken by a company relative to its commitment that is not externally verified, including data that is verified by a first-party.

- First-party verification: Verification conducted by the company itself but carried out by personnel not involved in the design or implementation of the operations being verified.

Externally verified: Assessment and validation of compliance, performance and/or actions taken by a company relative to a stated commitment, standard, or target.

- Second-party verification: Verification conducted by a related entity with an interest in the company or operation being assessed, such as the business customer of a production/processing operation or a contractor that also provides services other than verification.

- Third-party verification: Verification conducted by an independent entity that does not provide other services to the company.

Due to the wide range of people/organisations that might be involved with companies’ activities we have not put any minimum verification standards in place other than requiring the verification to have been done by a body separate from the company being assessed. However, all types of external verification will be assessed on a case-by-case basis for their suitability. For example, evidence of a company working with a local NGO on its satellite monitoring for deforestation would be sufficient for externally verified points. This could be evidenced through a report on the company’s website clearly produced in partnership with the NGO, including the use of its logo, or through linking to the relevant information on the NGO’s website. Other than requiring the scoring criteria to be met, we do not assess the quality of the externally verified information and encourage users to review this data and draw their own conclusions. This methodology aims to recognise the efforts of companies that are working with other organisations on sustainability projects, that may not be verified against a specific standard.

For several indicators in the palm oil, timber and pulp and natural rubber frameworks, companies are awarded additional points for the proportion of area/volume that is certified through RSPO, FSC or PEFC. Companies are still awarded points for self-reported progress and progress verified by other parties, but they receive additional points in recognition for their efforts in obtaining certification. This means that SPOTT not only considers membership of a certification scheme, but also the extent to which a company’s production or supply is certified.

SPOTT is not affiliated with any organisation offering verification services for SPOTT assessments and does not offer its own verification service.

Assessment Scores Explained

SPOTT provides assessments of palm oil, timber and pulp and natural rubber producers, processors and traders on the public disclosure of their policies, operations and commitments to environmental, social and governance (ESG) best practice.

The primary aim of SPOTT assessments is to provide a measure of a company’s transparency as it relates to ESG risks.

What is transparent information?

ZSL defines transparent information as information communicated by a company via publicly available materials that are freely and readily accessible to all stakeholders. ZSL considers transparency to be a vital first step towards sustainability.

We updated the SPOTT methodology in 2019 to reflect both the type of disclosure and the level of reporting and verification available. Together, this offers greater nuance to users and therefore supports more meaningful engagement between companies and their stakeholders.

What does a company’s score mean?

A higher score on SPOTT indicates that the company is being relatively transparent about its operations, policies and commitments to ESG best practice. Some SPOTT indicators also consider the quality of policies and commitments, with higher scores awarded for more comprehensive policies. Higher scores may also reflect company reporting and externally verified information on implementation

If a company receives a high score in its SPOTT assessment, this does not necessarily mean the company is itself environmentally responsible – just that it is being more transparent in its ESG reporting than other companies with a lower score.

We encourage all companies – not just those featured on SPOTT – to make their sustainability policies and commitments publicly available. Without such transparency it is impossible for third parties to evaluate their content, and thus, assess ESG risks or hold companies accountable. SPOTT also encourages companies to regularly report on their progress towards meeting their commitments.

However, a high level of company transparency does not necessarily mean that a company is sustainable in terms of its impacts on the ground. As such, SPOTT does not directly assess the implementation of policies and commitments.

Genuine and non-genuine score changes

SPOTT assessments rely on publicly available information. Though we take every care to capture all available information, there may be instances where we discover new information or reassess data, resulting in a non-genuine* change to a company’s score. Providing reasons for these changes helps users to identify when a company is genuinely improving:

Genuine reasons:

- New information publicly disclosed by the company

- Clarifications made by the company through the engagement and feedback process since the previous assessment

- Information that was publicly available is no longer accessible during the assessment period

Non-genuine reasons:

- Information missed but publicly available during the previous assessment period

- Reassessment of information originally provided by the company

- Correction of indicator framework and/or scoring criteria since the previous assessment

- Addition of new indicators within the framework

To track trends and score changes between assessments in more detail, visit the SPOTT Dashboard.

Going further: due diligence and verification

We urge SPOTT users to perform wider due diligence on companies, using SPOTT as the starting point. Such due diligence activities could include:

- Direct engagement with companies on missing commitments, and/or whether existing commitments are being implemented on the ground and in line with time-bound plans. SPOTT assessments can be used to identify existing commitments – including self-reporting of progress against certain policies and commitments – and to identify gaps in company policy frameworks and reporting.

- Review of the SPOTT media monitor, which gathers reports and stories from global media sources, covering specific company activities related to SPOTT indicator categories. The media monitor appears below the latest assessment on individual company pages.

- Review of research reports and investigations by civil society on the impacts of company (own and supplier) operations. When applicable, review SPOTT scores, media stories and reports for the companies’ suppliers.

- Inspection of external audit reports to identify areas of non-compliance, which may include second-party audit reports (usually conducted by consultants), and independent third-party audit reports of certification schemes (e.g. FSC, RSPO).

- Consideration of available spatial data to identify environmental risks associated with company operations (e.g. fire, deforestation, proximity of protected areas).

*based on a methodology originally developed for the International Union for Conservation of Nature (IUCN) Red List of Threatened Species.

Please read our FAQs or contact us if you have further questions.